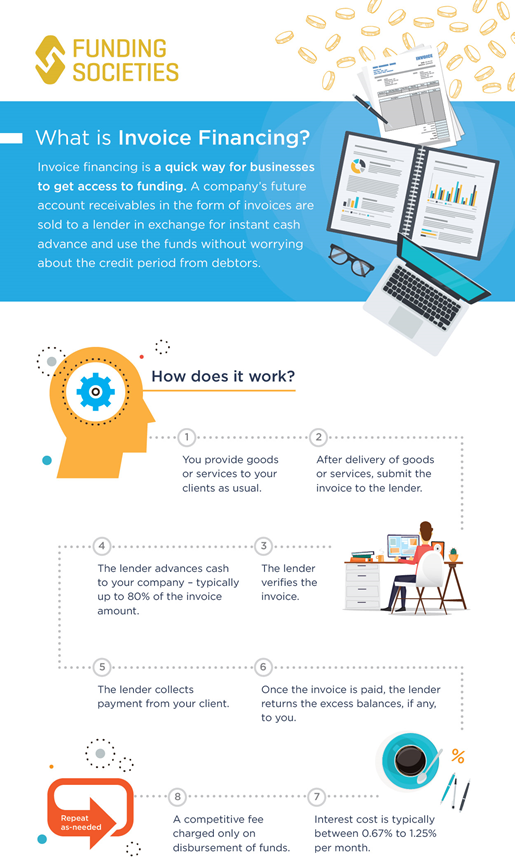

These days, there are several resources available for business loans. But while the options exist, receiving funding is never easy – especially if you are part of a small business. Then there’s the evaluation bit. Lenders review your application thoroughly before they can deem you worthy and disburse the necessary funds. (For more information on the loan evaluation process, see this article).

Obviously, you want to maximize your chances of loan approval. Ask yourself these question before you prepare your loan application:

-

Why do I need a business loan?

Every business loan consideration should start with this question. Do you really need a business loan? Of course, there are many excellent reasons why a business loan would be beneficial: you are planning an expansion and need financing to make it happen, you need to purchase equipment to improve your product, you need to purchase more inventory from your supplier, or you just need an injection of working capital.

Feeling unsure if your “why” passes the test? Here’s a good rule of thumb: ask yourself if a business loan will make your business grow. If the answer is yes, go for it. If not, you may want to evaluate some of your priorities.

Remember: whatever your reason for a business loan application, your lenders will question you about it. Be sure you can explain your reasoning eloquently.

-

How much money do I need?

Like question number 1, lenders will ask loan applicants this question. Do ensure that you have spent enough time making proper calculations. If you are buying equipment, research the cost. Create financial projections.

Asking for too little will create working capital problems and might make your company financials suffer. Asking for too much makes you look as if you haven’t done the necessary research. Worse, lenders may think you lack credibility.

-

How are my financials?

Obviously, your lenders will want to know if you can repay your loans. Otherwise why would they bother? So make sure you have a healthy cash flow and solid financial figures.

It’s very likely that you will be asked for your company’s balance sheets, income statements, cash flow statements, and bank statements so your lenders can analyze your situation.

Take the time to create accurate projections. Try to create a debt repayment plan as well.

-

Do I have other debts?

Related to number 3, lenders will want to know all about your credit history. They want to ensure that you can repay your loan, and if you have other unmet obligations hanging over your head, lenders will view your other debts as a danger sign.

-

Which lender is most appropriate for my credit needs?

Take the time to choose a lender that suits your needs. Research various loan products and structure, take a look at loan interest, etc. There are different lending institutions for different needs, such as large and small banks, financial institutions, government-backed loan packages, and alternative lenders, such as crowdfunding.

To read more about finding business financing for small businesses in Singapore, click here.

-

Do I meet my chosen lender’s requirements?

Business loan applications goes both ways. While you need to choose the most suitable lender for you, it is crucial that you meet their requirements. Otherwise, sending a loan application would be a waste of time. And it can hurt you, because the next lender you apply to might question why you were rejected for other business loans.

-

What’s my business plan?

Lenders will ask for your business plan. They want to know details on how you will use the loan money, what your plans for the future are, and whether you will ultimately repay your obligations.

A strong business plan should include past and current financial statements, along with future projections. Other elements you may want to consider are: company and product description, market analysis, and company strategy for growth.

-

Do I have all my documents in order?

If you have all your documentation ready, the application process will be much smoother. You will also look prepared to your lender.

While required documents vary across different lending institutions, every lender will ask for financial statements. In addition, you may be asked for your credit report (personal and/or business), tax returns, bank statements, collateral information (depending on loan type), and legal documents (business licenses and registrations, articles of incorporation, etc)

Ultimately, applying for a business loan is all about preparation. Good luck!