If it is long-term financial security you are after, you will have to start investing – and better sooner than later. In this post, we will focus on the types of available. Major instruments include:

-

Time deposits

A time deposit is a bank deposit with (i) a higher interest rate than a regular savings account, and (ii) a clear date of maturity. There are penalties for early withdrawals but once the account reaches maturity, you can withdraw funds without any fines. Or you can choose to leave your funds for another term. The longer you leave your money alone and the higher the amount of funds, the more interest you earn.

Time deposits are considered a low-risk, safe form of investment. It’s also easy to set up and is not complicated to grasp – so much so that time deposits are considered a beginner’s investment.

There are disadvantages, however. You can’t touch your funds during the term’s duration, so make sure you can afford to have your money locked away for the time being. Also, while a time deposit’s interest rate may be higher than a regular savings account, the same interest rate is lower than other types of investments and is in fact so low that time deposits’ rates often lose out to inflation rates.

-

Precious Metals

Gold is a classic investment that remains popular throughout Asia. There are differing opinions on whether or not gold is still a viable investment. For your reference, we will include three varying arguments: from Investopedia, from CNN Money, and from the Daily Telegraph.

In general, gold and precious metals preserve wealth against rising inflation. For a long time, they have been considered safe investments during political and economic upheavals.

However, gold prices are actually very volatile. Also, gold pays its owner no income, unlike say, bonds or dividend stocks.

-

Property

Property serves a similar function to gold: it is seen to preserve wealth against rising inflation. The value of property generally appreciates overtime, making property a popular long-term investment.

However, the main disadvantage of investing in property is glaringly obvious: entry cost is high. You need a lot of money to buy property. Additionally, property is not liquid and requires plenty of upkeep.

If you do have the resources to invest in property, you have options. You can hold on to your property and wait for its value to increase before selling it off for profit. Something else you can do is rent your property.

Renting your property is a great way to generate steady, passive income. However, you run the risk of ending up with a bad, destructive tenant. Or worse, no tenants.

-

Bonds

When companies and governments need funds – perhaps to expand, perhaps to build infrastructure, they can choose not to borrow money from banks. Instead, they can issue bonds. Basically, bonds are a form of debt where a corporation/government is the borrower, while you – the bonds buyer – are the lender.

For example, if you buy a bond with a face value of $1000, an interest rate of 6%, and a maturity of five years – that means you’ll consistently receive $60 of interest per year for the next five years. When your bond matures after five years, your $1000 will be returned to you.

Bonds are lower-risk investment, but provide lower returns than, say, stocks. However, bonds’ fluctuations are also less dramatic than stocks. In addition, like time deposits and unlike gold, bonds provide a stable passive income.

-

Stocks

Stocks are arguably the most well-known of all investments. Stocks are shares in the ownership of a company. When you own a company’s stocks, you have a claim on the company’s earnings – also called dividends. Stocks are popular for a reason: they offer higher returns than other instruments like bonds and time deposits. However, stocks are higher-risk investments, with prices rising and falling dramatically.

Ultimately, there are two types of stocks: dividend stocks and growth stocks. A growth stock is a stock in a quickly growing company. However, growth stocks pay back none of the company’s earnings as the growing company would rather use their earnings to expand their business. The only way you can make money from growth stocks is by selling off your stocks. Dividend stocks are the opposite. They pay stockholders part of the company’s earnings. The more dividend stocks you own, the larger your dividend portion.

While you can make money selling off excellent growth stocks, there is no guaranteed return. Meanwhile, dividend stocks replaces your income by paying you back in dividends. It all depends on your risk tolerance.

-

Alternative Investments

Traditionally, alternative investments include investments that are not in the traditional forms of stocks, bonds, and cash assets. Artwork, antiques, and precious jewelry are all considered alternative investment.

Once upon a time, alternative investments were more intended for the wealthy. After all, you need money to build a painting or jewelry collection.

However, the status quo is changing thanks to the development of financial technology. Forms of alternative investments are increasing. A notable example is peer-to-peer lending.

Peer-to-peer lending platforms match investors and borrowers via digital technology. Borrowers get loans with competitive interest rates and investors are consistently paid back in installments.

Compared to other forms of alternative investments, the entry cost to investing in peer-to-peer lending is low. Like bonds and dividend stocks, peer-to-peer lending is a good source of passive income. While it does carry risk because borrowers can default, a good peer-to-peer lending platform will have performed the necessary due diligence.

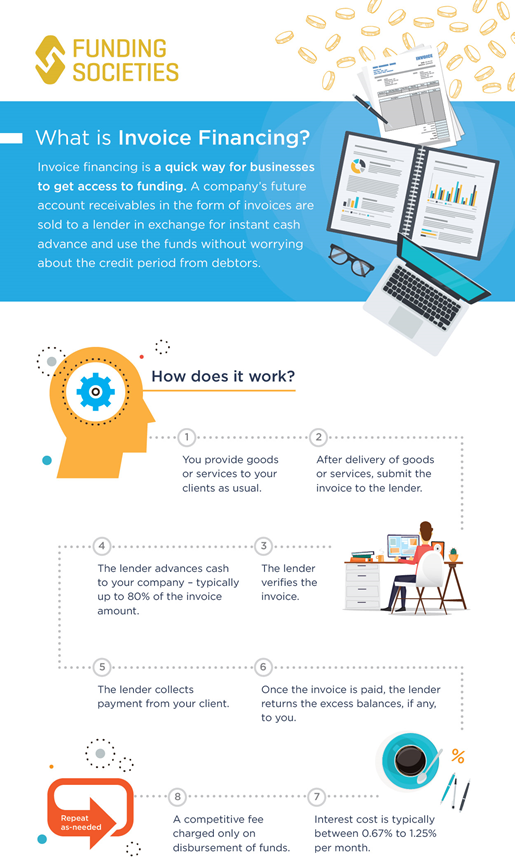

Find out more about Alternative Investments through Funding Societies here.

Funding Societies is a DollarsAndSense Brand Connect partner. If you are interested to know them better, you can find out more on what they do on our DollarsAndSense Brand Connect Page.